Sub-4% Mortgages at Risk: Inflation Surges Beyond Expectations in Canada

The most affordable mortgages available might be "at risk" following these developments. Inflation rose to 3.5 percent. based on the most recent official data.

The rise in inflation was anticipated to go up from 2.6 percent. However, the magnitude of this change surpassed economists' forecasts, resulting in restrained expectations for quick interest rate reductions.

The speed at which interest rates are expected to decrease significantly influences swap rates – an essential element thereof. mortgage pricing —and have noticed some lenders increasing their rates.

This has caused brokers to say that "it wouldn't be unexpected" if additional rate increases occur.

Read Next: The four actions Rachel Reeves could take to reduce inflation

In recent six weeks, fixed-rate mortgage prices have decreased significantly, largely due to economists anticipating that the substantial tariffs imposed by Donald Trump on imported goods into the U.S. could weaken the American economy and consequently lower UK inflation rates.

However, the effect of these tariffs is anticipated to be considerably smaller following the withdrawal or postponement of numerous scheduled duties.

This, along with the inflation data released on Wednesday, indicates that multiple interest rate reductions in 2025 are now highly uncertain.

Rob Wood, who leads as the chief UK economist at Pantheon Macroeconomics, stated, "Given the surge in inflation to 3.5 percent, the Bank of England will find it challenging to reduce rates two more times this year."

Sanjay Raja from Deutsche Bank Research commented, "It’s highly probable this marks the end for a potential interest rate reduction in June. Although we believe an August decrease remains plausible, the situation has grown considerably more intriguing and evenly weighted."

Several mortgage providers have begun increasing their interest rates in recent days. Both TSB and Halifax have made these changes lately, with expectations that others will likely do the same soon.

By how much are mortgage rates anticipated to increase?

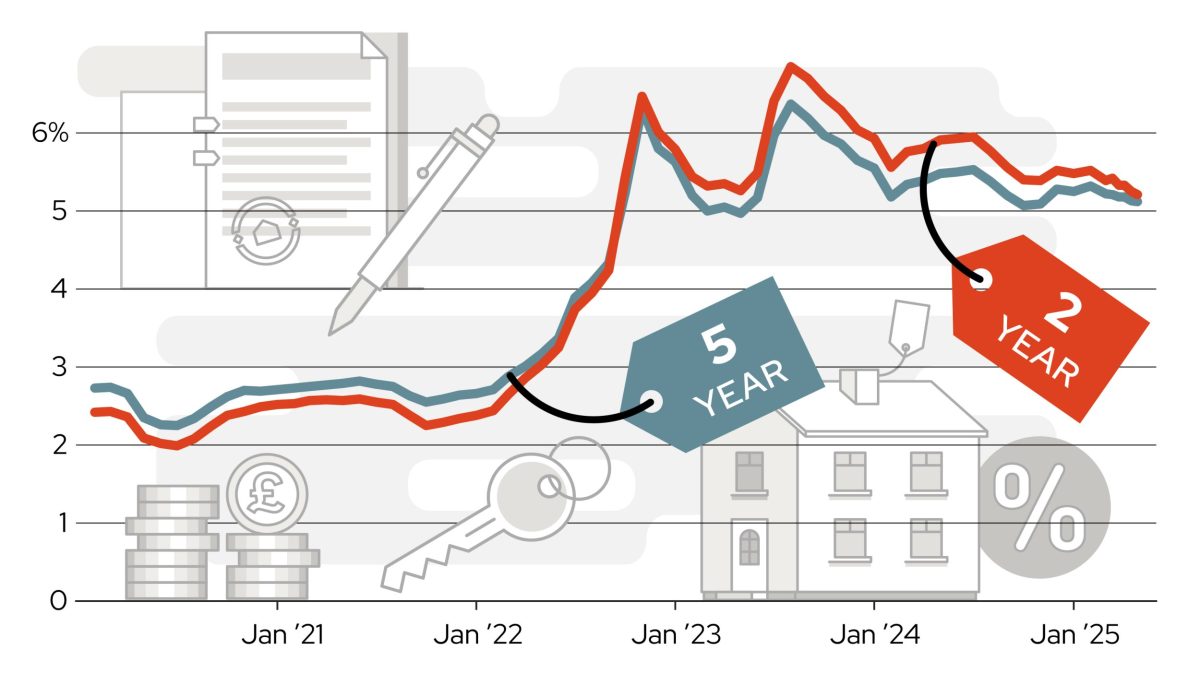

The most affordable rates available − intended for individuals who have substantial initial payments or significant equity in their current homes − currently stand at approximately 3.8 percent; however, these might rise nearer to 4 percent and may potentially exceed that level.

The typical rates for two and five-year fixed terms stand significantly higher, at 5.11 percent and 5.07 percent respectively, as reported by Moneyfacts.

David Hollingworth of L&C Mortgages, said: “Those cheapest rates were already under threat – the inflation figure will add to that feeling.

The significant decrease in interest rates followed tariffs imposed by the U.S., and the fear of further such actions has somewhat subsided. However, some financial institutions are raising their rates again, which could lead to slight upward adjustments in the lowest available rates.

Nick Mendes, the mortgage technical manager at John Charcol, stated: "Several top deals available right now could be jeopardized if swap rates continue to stay at their present levels, since there isn’t much—or any—room left for reducing margins."

Deals below 4% might also be endangered if future developments modify predictions or lead to a shift in policy from the Bank of England.

Aaron Strutt from Trinity Financial commented, "Given the recent inflation numbers and higher funding costs, an upcoming hike in mortgage rates wouldn’t come as a shock. We’ve already observed TSB and Halifax increasing certain fixed-rate offerings."

If you're considering taking out a mortgage in the near future or require refinancing, I'd recommend trying to secure one of the more affordable options available.

Several mortgage providers have cautioned that interest rates might go up.

Peter Stimson, the director of mortgages at MPowered, cautioned: "Currently, mortgage rates have reached their lowest point and we might observe them gradually increasing in the coming weeks as lenders adjust their prices in reaction to climbing swap rates."

Increased mortgage costs would deal a significant setback to the government.

One factor contributing to rising inflation is the increase in national insurance contributions made by employers. Many businesses have offset this cost by raising their prices.

When asked whether the inflation numbers were increased due to the measures in her budget from last October, Chancellor Rachel Reeves stated on Wednesday: "I understand that every policy comes with consequences; however, if I hadn't taken action to stabilize public finance, our situation would be even more dire now."

Ways to Combat Increasing Mortgage Rates

When purchasing a house...

If you submit an application for a mortgage and get a formal offer, many lenders permit you to secure that interest rate for a set duration, usually ranging from three to six months, during which time you finalize your home purchase.

Several lenders extend validity periods of up to nine months, especially for instances related to new constructions, as these often require more time to finish.

When your mortgage is nearing completion...

Should your mortgage be set to expire later this summer, you have the option to take action now in order to lock in a favorable low rate ahead of time.

Should interest rates decrease, you may be able to switch to a more affordable option prior to your present agreement ending. Lately, many lenders allowed customers to secure new rates up to six months ahead of their current deals concluding; however, this policy seems to have been revised lately.

“As lender timeframes have evolved, what was once a six-month period for securing a new deal has shortened to about three or four months due to increased market stability,” says Justin Moy from EHF Mortgages.

{kind=link}

Post a Comment for "Sub-4% Mortgages at Risk: Inflation Surges Beyond Expectations in Canada"